Introduction

Our worldview and investment philosophy

Generation is a pure play sustainable investment manager – it is all we do, and all we will ever do. We see long-term investing as best practice and sustainability as the organising construct of the global economy. We use Environmental, Social and Governance (ESG) factors as tools to evaluate the quality of business and management. We believe this approach reveals important and relevant insights which other investment frameworks may miss, and which ultimately leads to superior1, risk-adjusted investment results.

Generation has been investing in global equity markets for 16 years and in private markets for over 12. As of 27 April 2021, Generation has four investment strategies: our Global Equity and Asia Equity strategies in the public markets, and our Growth Equity and Long-term Equity strategies in the private markets. We operate as one firm, with a shared research platform and control environment across all strategies. Consideration of climate change-driven risks and opportunities has been core to Generation’s investment philosophy since its founding and is part and parcel of how we integrate sustainability factors into our investment process.

From the start of our journey, we recognised the need to build greater awareness of climate-related assessment among financial and non-financial companies alike. As such, we have helped launch and support several initiatives that accelerate the transition to a more sustainable economic system. In 2016 we were part of the founding membership of the Task Force on Climate-related Financial Disclosures (TCFD), which has been a key partner in our work to advocate for tools and frameworks to standardise disclosure.

In recent years, Generation has aligned its approach to assessing climate-related risk and opportunity across our strategies with the TCFD. This year, we are pleased to share our first integrated, firm-level TCFD report. Incorporating the TCFD’s guidelines was a natural next step in our evolution towards best-in-class climate risk assessment and reporting.

Furthermore, in 2020 Generation committed to aligning the investment portfolios we manage with net zero emissions by 2040. We made this commitment to our clients because leadership on the climate crisis is critical, and we believe that managing climate risk and opportunity is inseparable from our fiduciary responsibility. In the months following our commitment, we worked with peers and partners to establish a new Net Zero Asset Managers initiative (NZAM), a coalition of like-minded managers committed to supporting the goal of net zero emissions by mid-century. We believe that ensuring the integrity of net zero investing, reporting our progress against the TCFD framework, and encouraging our peers and our portfolio companies to do the same, is essential to industry-wide progress.

Consistent disclosure of climate considerations is the key to enabling all companies, managers and owners to assess their own exposure and opportunity. We look forward to continuing to learn and collaborate alongside our portfolio companies and peers in accelerating a long-term, sustainable transition.

Governance

Generation has established a governance framework designed to allow investment management, business development and client relationships, and operational control and risk management to be independently reviewed through a number of committees and oversight groups. A key element of the design of the risk management function is to ensure functional and hierarchical separation between the portfolio management, investment teams, and the control and compliance functional teams. The key sponsor of the governance and the control and risk management environment is the Senior Partner, who has a role similar to a Chief Executive Officer. He is supported and monitored by a committee structure as follows:

> The Management Committee (which is the firm’s governing body);

> The Remuneration Committee (which implements the Remuneration Policy);

> The Risk Oversight Group (ROG) (which provides focused support and governance on risk matters);

> The Valuation Oversight Group (which implements the Valuation Policy);

> The Operating Committee (which serves as the oversight group to business heads, who handle daily workflow and manage risk events); and

> The Conflicts Committee (which reports to the Management Committee and Risk Oversight Group on conflict management issues).

Leadership oversight of climate-related risks and opportunities

The Management Committee provides a forum for the partners to ensure that the business is being run in accordance with the Partnership Agreement. It oversees resourcing and strategy, including the management of climate-related risks and opportunities. Given Generation’s mission and its integration of sustainability research into investment processes, climate-related issues are always considered when developing strategy, overseeing risk and setting our performance objectives. The Management Committee maintains ultimate responsibility for the integration of climate consideration into our business processes.

The majority of the firm’s Management Committee have been with Generation since its founding, and several members have expertise in climate science, climate policy and the associated implications for businesses. For example, our Chairman is also the founder of the Climate Reality Project, which seeks to promote education related to climate change. Over Generation’s 17 years, the Management Committee has been critical in developing our integrated investment process and shaping the firm’s research and advocacy agenda with respect to climate.

Across every business line of the firm, business unit heads are also responsible for confirming the risks that they are exposed to within their respective groups and reporting this to the ROG via a central risk register. These risks include potential exposure to climate-related considerations, and results will be reviewed annually by the ROG and communicated to the Management Committee when necessary.

With respect to Generation’s own operational footprint, Generation’s Environmental Management System (EMS)2 is internally reviewed by the COO and assessed by the Operating Committee, with more frequent postings on specific events as they occur. The Management Committee reviews the EMS on a quarterly basis to appraise a summary of findings relating to completed actions, updated aspects and impacts or improvements made. The EMS is reviewed by external auditors on an annual basis. The Risk Oversight Group and Management Committee receive annual updates on the firm’s carbon compensation programme, with a focus on recommended reduction targets, suggested carbon compensation inclusions and progress of the projects supported by the purchase of carbon credits.

Our commitment to net zero by 2040

In July 2020, Generation committed to aligning all the investment portfolios we manage with net zero emissions by 2040. We made this commitment to our clients because leadership on the climate crisis is critical, and we believe that managing climate risk and opportunity is inseparable from our fiduciary responsibility. In the months following our commitment, we worked with peers and partners, in particular the Institutional Investors Group on Climate Change (IIGCC), to establish a new Net Zero Asset Managers initiative (NZAM) – a coalition of like-minded managers committed to supporting the goal of net zero emissions by mid-century.

The initiative now has 73 signatories from around the world, with a combined USD 32 trillion of assets under management, recruited through the work of several groups, including IIGCC and Ceres, and with the support of the High-Level Champions for Climate Action, which our Foundation has continued to support. As a signatory to NZAM, we are committed to publishing TCFD disclosures annually, including a climate action plan, and submitting them to the Investor Agenda via its partner organisations for review; to ensure the approach applied is based on a robust methodology consistent with the UN Race to Zero criteria, and that action is being taken in line with our commitments.

Embedding sustainability across our investment teams

Our investment leadership and teams are resourced with sufficient analysts to allow for the integration of sustainability research within fundamental equity analysis and the deep stewardship of all companies in which we invest. Our teams focus on what a given business does, as well as how the business operates.

For example, our public equity analysts cover a relatively small number of companies each – typically around 12. This permits each analyst to develop insights, gain conviction and undertake stewardship activities that others without similar levels of resourcing may find difficult to achieve. Because of the intense coverage of a company by our analysts, we expect to understand our stocks better than most managers, and to have a higher level of engagement with the management team and board. Although analysts are focused on different sectors, our approach is teambased, and constructive dialogue and idea-sharing across the team are valued and encouraged. Issues relating to climate-related risk and opportunity are routinely discussed at investment team meetings.

In our private equity teams, we use sustainability research as the lens through which we identify great business models and management teams. In taking a “system positive” approach, we look to ensure that firms’ services and products clearly drive a transition towards a more sustainable future. This requires that we characterise the first and second order implications of sustainability trends – which necessarily include the climate-related risks and outcomes. Across our Growth Equity team, all our investment professionals fuse fundamental analysis and sustainability analysis into an integrated approach to help identify, source and ultimately invest in attractive companies. In examining what a business does, we assess specific environmental, social, health and financial inclusion metrics at the point of investment, which we trust will drive performance.

We also have a dedicated Research Strategy sub-team focused on performing primary research, which supports our investment teams in assessing climate-related risks. The team manages relationships with traditional equity research providers, ESG research and climate data providers, and expert networks.

Finally, we have added several new roles to strengthen our monitoring and engagement on climate related issues. In 2020, we appointed ourfirst Director of Engagement. This new role enhances our ability to structure and undertake more ambitious engagement programs, use voting strategically in support of our investment objectives to accelerate climate action, collaborate more effectively with other investors and escalate engagement where necessary. In 2021, we appointed a Director of Research for our Growth Equity strategy to ensure that analysts and portfolio companies can access the best research and advisors, and communicate the strength of the platform. This role is also responsible for shaping research strategy for the team, including with respect to climate-related risk monitoring and reporting.

Strategy

Climate and our investment philosophy

Consideration of climate-related risks and opportunities has been embedded into our investment approach across all strategies since the firm's inception. In our view, the financial materiality of climate change has grown at a relentless pace since the firm was founded. We believe that the transition to a net zero economy is accelerating and resource efficiency solutions will drive productivity and profitability. We also believe businesses that are adapting to this transition will remain profitable over the long term, as will those businesses whose products and services directly meet impending resource challenges.

We consider climate risk both in terms of Business and Management Quality in our investment process, and seek to invest in businesses that are well-positioned for the net zero transition. Such risks may include carbon stranding through increased direct and indirect regulation; increasing competition from renewable technologies as they become economically viable and increasingly widespread; and socio-political pressures as emissions implications become less acceptable publicly.

Integrating this view into our Global Equity and Asia Equity portfolios has led us away from high carbon-intensive sectors such as oil & gas, coal, mining, cement and steel. The carbon intensities of our Global Equity and Asia Equity portfolios are less than 1/4 those of their respective benchmarks (MSCI World and MSCI All Country Ex-Japan, Scope 1+2) - partly for this reason, as well as positive selection within sectors.3

Identifying climate-related risks and opportunities

Roadmaps and research

Our sourcing is informed primarily by our research “roadmaps” that identify macro and sector trends, including material sustainability risks and opportunities. The development of roadmaps provides an opportunity for analysts and the broader investment team to investigate factors driving sector and global trends, while deepening their understanding of the investment landscape. Roadmaps may have a broader focus on countries or sustainability themes (e.g. water), but more typically focus on sectors and sub-sectors. Roadmaps allow the investment team to identify sustainability risks and opportunities that are relevant and material to particular sectors. Example research roadmaps include electric vehicles, the future of work, electric utilities, and so forth. In our roadmap on utilities, we evaluated the risks posed to utilities by impending climate-related legislation, the impacts of stranded asset risk, and the infrastructure challenges of a rapid transition to a dynamic, low-emissions grid.

Over the years, we have completed several hundred roadmaps across our public and private equity strategies, and for each of these have characterised the relevant short- and long-term climate considerations and drivers when material

Sustainability factors in company selection

Guided and informed by roadmap research, analysts pursue in-depth company research. This stage is structured around the robust criteria we have set for Management Quality (MQ) and Business Quality (BQ), as described below, which enable us to evaluate both what a business does and how the business operates. Aspects considered include barriers to entry, business stability and alignment of management incentives.

The criteria also necessitate a deeper analysis of the company’s positioning with regards to the material and relevant sustainability factors within its sector. Critical sustainability factors analysts consider pertaining to climate include:

> whether the company’s offerings impair or improve the present and/or future wellbeing of society;

> what externalities exist and who else might be “paying a price”;

> whether there are environmental or social vulnerabilities to be tracked.

Our private equity teams also overlay scrutiny of the company’s products and services with whether they accelerate a given sector to a more sustainable end-state. A key component of our private equity process is to ensure, in the earliest stages of diligence, that the business is system positive, which requires that its services and products clearly drive a transition towards a more sustainable future. To determine whether a company meets this threshold, we compile information about the total effects of a business model on people and planet, both positive and negative, including intended and unintended effects. This analysis encompasses the following areas:

1. System: whether the business model advances a transition towards a more sustainable economy

2. Environment & resources: lifecycle assessment to determine the first and second order environmental impacts of the business

3. Social & health: the net social and health outcomes associated with business growth, including implications for users and for the broader population

4. Operations and management: whether the company is driven by a strong mission, and how that is translated into operations, management, and culture.

The investment team debates aggregated data on how a company provides a net contribution to a more sustainable economy. Where possible, we use a lifecycle assessment approach to benchmark company performance against an appropriate baseline, which is particularly well suited to assessing environmental technology companies. For a business model with social or health-related business outcomes, the investment team compiles a net contribution assessment compared to a baseline. This enables us to focus our efforts on businesses we believe are providing true systemic solutions to material global challenges such as climate change, healthcare, income inequality and wellbeing.

The resilience of our strategies under different climate scenarios

Global Equity

We have always stressed the risks and opportunities of climate change as part of our investment process and have explicitly sought to structure our portfolio to be well-positioned for a low carbon transition. Carbon intensity is a gating consideration to a company’s inclusion on our Focus List, and our analysts often focus on modelling a specific aspect of the transition (for instance, the cost curves of battery storage). To this end, over the course of 2020 we partnered with Vivid Economics to explore the implied temperature rise of the Global Equity portfolio and the value at risk (or implied opportunity) under different scenarios for each of the sectors we cover. When we began this work, we knew there were aspects of current methodologies that do not apply perfectly to Generation, given our deliberate exclusion of high-carbon sectors. There are also limitations on how far existing methodologies can capture our own view of the downstream positive impacts of our companies. In 2021, we will work to refine our methodology and expand our analysis to incorporate strategies beyond Global Equity. Our findings from our initial 2020 analysis are shared below:

1. The Generation portfolio is aligned with a 1.5C pathway, in a preliminary analysis. The results tentatively indicate that the portfolio is aligned with 1.2°C of warming to 2100 compared to 3.1°C for the MSCI ACWI – on a Scope 1 basis. However, this methodology covered Scope 1 only, to avoid double counting. This is a material deficiency in the analysis, as greenhouse gas emissions associated with many of our companies are predominantly Scope 3. In our next iteration, we will incorporate Scope 2 and, if possible, Scope 3 emissions to improve the accuracy of this analysis. So, while we would certainly not wish to place reliance on this analysis at this stage, we hope it is indicative of the direction of travel.

2. While the MSCI ACWI loses 4% of current valuation under a 1.5C scenario4, the Generation portfolio gains 1% in value. We are excited by this initial result, as it is very much in line with our broad investment thesis. We would caution though that it is very much a preliminary analysis and there is no guarantee this result will be achieved. The assessment is based on a different, sector-by-sector assessment that seeks to identify the climate value at risk in the portfolio. It captures a portion of value chain emissions by considering the impact on sales of green goods

and services.

3. Increase in demand for low carbon products is more important for Generation’s portfolio compared to the MSCI ACWI, where demand destruction plays a greater role. Generally speaking, across the broader MSCI ACWI Index some companies lose more than others, as a result of higher carbon prices and shrinking markets for their products. There are few gainers. The striking difference for our Global Equity portfolio is that it appears to suffer little demand destruction and benefits from growing markets for technologies like electric vehicles and energyefficient lighting. Exposure to carbon costs is much smaller and, importantly, emissions are largely dealt with through abatement (actual emissions reductions) rather than passing the carbon costs onto customers and continuing to pollute.

These findings are consistent with our own analysis and the general picture is supported by some of our companyspecific assessments. However, we would encourage caution in interpreting the precision of the numbers at present.

Growth Equity

As mentioned above, our Growth Equity strategy exists to back businesses driving the transition to a more sustainable economy. Our foundational roadmap work across industries (including energy, transport, industrials, food and agriculture, the built environment, and other areas) is where we articulate our understanding of what is required to align to a 1.5C scenario, and the associated risks and opportunities. In our coverage of environmental technologies, we seek to back those companies with products and services that displace less efficient incumbent solutions (for example, non-animal protein to displace meat or electric transport to displace internal combustion engines). We leverage lifecycle assessments to ensure a net reduction in emissions relative to business as usual. In our coverage of healthcare and financial inclusion businesses, we seek to address health and social outcomes that improve wellbeing and address inequality, both of which are critical to achieving the UN Sustainable Development Goals aligned with a stable and inclusive net zero economy by 2050. In all cases, we require that our portfolio companies monitor and report on their Scope 1, 2, and 3 emissions to demonstrate alignment with net zero commitments.

In terms of scenario planning, our entire focus within the Growth Equity platform is on achieving a pathway aligned with 1.5C, and our portfolio companies should be enablers of that future. However, through our roadmap work we also look to understand the IEA and IPCC scenarios where we do not achieve the Paris target – in one recent example, we centred this analysis on a 3C world. In that context, we review the nature of climate-related risks and challenges to our companies as a function of the geographical locations of a company’s supply chain, the nature of its operations, the impact that an accelerated climate-warming scenario would have on the structure of its market, the impact on supply and demand of its products or services, and the impact on its customers and associated communities

Climate and our operational philosophy

Our firm’s direct environmental impact and associated climate risk exposure is primarily driven by the operation of our offices and business travel. We aim to minimise our carbon footprint and use of environmental resources through our sourcing decisions and our carbon compensation program, as well as through promoting behavioural changes amongst our employees, suppliers and other stakeholders.

Our offices

Our most significant operational consideration is that of our offices, in London and San Francisco. In light of the COVID-19 pandemic, we have transitioned our technology and infrastructure in such a way to support a fully remote work environment. While we look forward to returning to our offices, we are no longer operationally reliant upon them to work at full capacity.

Generation has consciously designed its offices to minimise the environmental impact of its operations. Both are centrally located and well-served by public transport facilities. In London, our office at 20 Air Street achieved an “Excellent” rating by BREEAM (Building Research Establishment Environmental Assessment Method). In addition to a rainwater harvesting system, an intelligent lighting system is in place to maximise natural light and limit wastage. A biodiverse sedum roof improves insulation and supports the local bee population. The interior modelling has the “SKA Gold” rating. Similarly, our San Francisco office is located in a building which has been successfully re-certified as “Platinum” for its LEED-EBOM rating, which applies to existing builds. Our own fit-out received “LEED Platinum” certification. We used sustainable and non-toxic products and materials, adhering to the WELL standard with its primary focus on the health and wellbeing of occupants. Both our London and San Francisco offices have on-site processes for the separation, collection and recycling of different types of waste materials, including food waste. Both also work with building management on an ongoing basis to prioritise energy efficiency and sustainable practices. We were awarded “WELL Gold” certification in San Francisco and are currently pursuing the same standard for our London office.

Suppliers, training & monitoring

Business-related sourcing decisions also include local travel and office supplies, where we choose sustainable

suppliers as much as possible, which in turn aims to minimise possible climate-related risk. We assess our suppliers against a checklist, which includes questions relating to their own ESG practices. As part of the induction for new joiners, we communicate the environmental practices we have in place for recycling and provide training on the energy-saving decisions individuals can make and the relevant technology available. We aim to engage local suppliers where possible, or those that already service our building, with the aim of reducing travel and consolidating deliveries. In 2020 we implemented an internal Environmental Management System (EMS), which provides us with a framework to monitor resource use, reduce waste, mitigate environmental risks and improve our sustainability efforts.

Carbon compensation

Generation is committed to carbon compensation for what we see as the unavoidable carbon emissions of our

business activities on an annual basis. While we strive to manage our usage and sourcing decisions, we recognise the constraints inherent within necessary business travel, especially air travel. We base our measurement of the firm’s carbon footprint on our business travel and office use, as well as the carbon emissions created by the households of Generation team members. We consult with third parties to apply widely accepted emissions factors to measure our travel, energy use and household data. Whilst we appreciate that carbon credits do not provide a complete solution, they contribute to mitigating our overall environmental impact while we work to reduce our emissions to as close to zero as possible.

Advocacy and impact initiatives

Generation was established in response to the concerns of its founders about the detrimental impacts and systemic risks posed by short-termism and the failure to integrate sustainability considerations into investment analysis and stewardship. Working to address these challenges is intrinsic to Generation’s purpose and our vision of how to mitigate systemic climate risk.

As a small firm with big aspirations, we must focus, motivate and collaborate with others. We pursued the following impact initiatives in the past year to leverage our track record, differentiated approach to investment research and convening power:

Research

> Sustainability Trends Report (STR): drawing on more than 190 sources, we published our fourth annual STR in 2020 and hope it will become the “go-to” resource for those seeking information on sustainability developments. Our aim is to aggregate and share insights that governments, businesses and investors can use to ensure a healthier, safer and more equitable world.

> Sustainability Insights: we launched our Insights series to share lessons drawn from our investment work in the form of publicly available research papers. In 2020, we published two papers aimed at helping to raise the bar on sustainability: Ecommerce vs Bricks & Mortar and System Positive.

> Measuring Portfolio Alignment: to meet growing investor and lender interest in measuring the alignment of financial portfolios to the objectives of the Paris Agreement and to advance the adoption of a consistent and © GENERATION INVESTMENT MANAGEMENT LLP 2021 Page 9 robust approach, Generation chaired a private sector initiative to critically assess the range of approaches for measuring net zero alignment of companies and investment portfolios. In November 2020, the Portfolio Alignment Team published its findings in a report, available here on the TCFD Knowledge Hub.

Collaboration & Advocacy

> The Generation Foundation: the Foundation has matured and developed since its inception 15 years ago. In earlier years, the Foundation’s role was to introduce and explain sustainable investment to a wider audience. In 2020, the Foundation entered the next phase of its work with targeted action in areas that contribute to two related impact goals: limiting global warming to 1.5 degrees Celsius and creating fairer, inclusive economies. The Foundation now has a portfolio of around 20 strategic partnerships. The Foundation is the largest donor to the COP26 Non-State Actor Champions office and supports their work to galvanise business and civil society efforts on climate and build a groundswell of ambition at the most important COP yet.

> Investor Engagement: we sought to leverage our client relationships and use our convening power to hold a series of asset owner gatherings to build momentum in the lead-up to COP26. In 2020, we hosted two gatherings with the aim of sharing information about portfolio alignment tools, company engagement and the case for urgent and transformational capital allocation to achieve net zero emissions. We conducted a series of four convenings and leveraged our relationships with asset manager peers to help establish the Net Zero Asset Managers initiative, a coalition of managers willing to make a collective commitment to the goal of net zero emissions by 2050 or sooner.

> Natural Climate Solutions (NCS): to achieve net zero, we must reimagine our relationship with nature. Today’s approach to land use and agriculture is a major source of greenhouse gas (GHG), biodiversity loss and exploitation. A fundamental change and scaling of natural climate solutions (NCS) have the potential to deliver more than 30% of the emissions reductions required for net zero.5 This transition is less well understood than those in sectors like energy and transportation. Consequently, Generation has started working with New Forests, a specialist in sustainable real asset investing, together with Conservation International, The Nature Conservancy, World Resources Institute, Ceres and others to mobilise more investor resources into NCS. Our kick-off convening in February attracted 35 asset owners representing USD 10 trillion in assets, and we are eager to accelerate attention and capital deployment into this promising area.

Innovation

> Climate TRACE: the Climate TRACE (Tracking Real-Time Atmospheric Carbon Emissions) coalition is building the world’s first tool to identify, quantify and trace all significant human-caused greenhouse gas emissions to their sources in real time, using space-based images and data from existing satellite constellations alongsidedata streams from land-, sea-, and air-based sensors; combined with artificial intelligence and machine learning. When activated in the summer of 2021, this tool is designed to bring radical transparency to the global dialogue under the Paris Agreement. In 2020, Generation helped to launch Climate TRACE through a USD 3 million grant.

> Just Climate: Generation is excited to be launching Just Climate, a climate-led investment business that will be an independent subsidiary of Generation. Just Climate’s mission is to identify, catalyse and invest in solutions that will help achieve net zero and 1.5 degrees through a “Just Transition”. Just Climate seeks to be transformational - by investing in companies that can accelerate and catalyse the scaled deployment of high impact technologies, projects and hard assets.

Risk management

Our approach to identifying risks

Evaluating climate-related risks (and the resulting opportunities) is core to all our investment strategies, as described in the previous section with respect to our research roadmaps, our company selection process, and how we expect to evolve our strategies under various climate scenarios.

For each of our strategies, we track a wide range of sustainability indicators at the portfolio company-level and hold regular monitoring meetings with companies. We have identified sustainability factors material for our investments and operations through comprehensive external and internal stakeholder engagement and materiality assessment, aligned with the UN-backed Principles for Responsible Investment, the Net Zero Asset Managers initiative, the Task Force on Climate-Related Financial Disclosures and the UK Stewardship Code.

With respect to our internal operations, business unit heads are responsible for tracking the risks that their individual teams are exposed to within their respective groups. This is documented within a central risk register, which the ROG has a responsibility to oversee. Building on our existing process, we will look to introduce more granular assessment of climate-related risks in the coming year, although we recognise that given our small employee base and footprint, our greatest potential exposure to climate-related risk lies with our investment strategies.

Engagement on climate risks and opportunities

Global Equity & Asia Equity

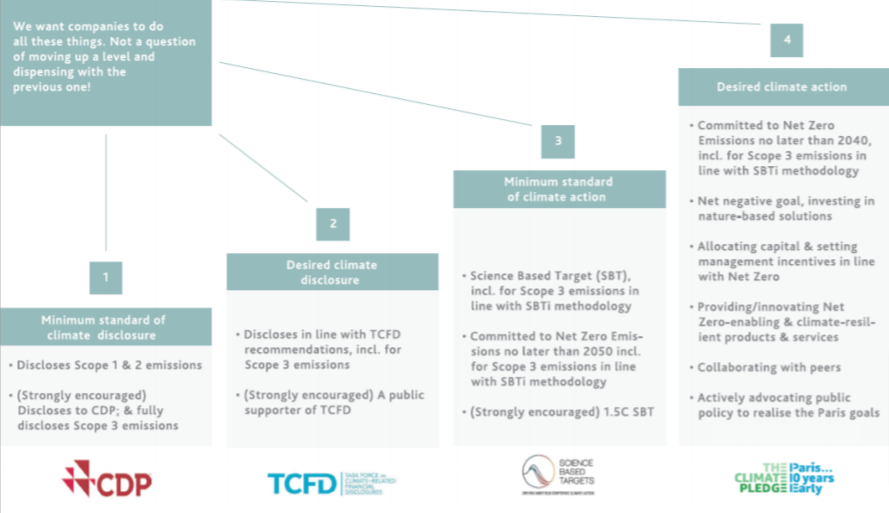

In the second half of 2020, Generation agreed upon a new framework for climate change engagement. In the diagram below, we lay out four levels for engagement. We aspire for companies to ascend these levels as quickly as possible. At Level 1, companies disclose their greenhouse gas emissions either to the Carbon Disclosure Project (CDP) or in annual reports. At Level 2 they have disclosed on climate-related risk and opportunity, in line with the recommendations of TCFD. At Level 3, the company has set a science-based target. And finally, at Level 4, companies are actively demonstrating leadership on climate action.

At the end of 2020, we wrote to all Focus List companies tracked by our Global Equity team to introduce our climate engagement framework. We used this opportunity to share detailed resources and to deepen our support of companies at every level, from those beginning to monitor and report emissions to those looking to attain best practice.

At the same time, we made clear that our expectations on climate change would increasingly impact our investment and voting decisions, given our conviction about the importance of sustainability factors in driving business performance and our own commitment to achieving net zero portfolio emissions by no later than 2040.

These activities laid the groundwork for our engagement on climate change in 2021. From our Focus List of companies, we identified high priority targets for engagement – those companies that are non-disclosers, material emitters or businesses we believe have the greatest potential to be system positive on climate change.

We have taken a slightly different approach to our Asia Equity strategy. While all Asia Equity companies on our Focus List received our climate engagement framework and resources, we also recognize that Asian companies to date have been less focused on climate-related disclosure and action than their global peers. In 2020 we focused our efforts on a smaller subset of large Asian companies which we believe have the potential to be Asian champions for climate action.

Growth equity

Within our Growth Equity strategy, we are focused on supporting companies that are already system positive – which drive, in many cases, the scale-up of climate solutions that in fact mitigate exposure to climate risk. As an example, we invested in Convoy. Launched in 2015, Convoy has built its industry’s first digital freight network, moving tens of thousands of truckloads per week in the U.S. In this new model the pricing and matching of shipments to carriers happens automatically, and machine learning is used to evaluate all shipments and carriers simultaneously to match the right job to the right truck. According to the EPA, heavy-duty freight accounts for more than 205 million metric tons of CO2 emissions per year, equivalent to 13% of total US vehicle emissions. Convoy’s Automated Reload program reduces empty miles from the industry standard of 35% to 19% by bundling shipments. If the entire industry were to achieve the same efficiency, Convoy estimates it would lower CO2 emissions by 32 million metric tons, equivalent to taking 6.9 million passenger vehicles off the roads for a year. In light of this opportunity, Convoy has become a key partner to companies like Waiākea, CHEP, and Anheuser-Busch in achieving their own sustainability targets. A Generation partner sits on the board of Convoy and is actively engaged in supporting their growth.

In addition to our engagement with portfolio firms, the Growth Equity team regularly collects and reports impact data to monitor climate-related risks. Generation has developed a bespoke framework based on best practice measurement and reporting protocols (including those outlined by the Sustainability Accounting Standards Board, the Impact Management Project, and others) and works with each portfolio company to evaluate critical ESG risks and opportunities on an annual basis. This also includes annually assessing the portfolio’s Scope 1, 2, and 3 emissions.

Long-term Equity

Generation’s Long-term Equity team holds one portfolio investment, FNZ, a global investment platform providing multi-channel wealth management services. FNZ is a signatory to the UN-backed PRI, the UN Global Compact, UNEP FI and the UN Green Digital Finance Alliance, and furthermore has announced its ambitions to repay all its historic carbon debt by 2025. The pathway to achieve this involves identified operational changes (including travel, procurement, behaviours) as well as offsetting unavoidable emissions. Climate and governance risks are integrated into operational risk and resilience planning at the business level.

Additionally, we believe the challenges associated with climate change are on one level an issue of capital allocation. Providing tools and services which can help influence institutional and retail capital allocation into more sustainable pathways will be a critical component of addressing the climate crisis. We believe FNZ has the potential to catalyse sustainable capital allocation through its “FNZ Impact” product and through partnerships for change. FNZ Impact delivers a range of individually tailored sustainability analytics and services to investors, who can then understand and address what matters to them, whether it be their portfolio carbon footprint, nature or diversity in the workplace.

They will be able to access the environmental and societal impact of their portfolio and consider the extent to which their investments help address the world’s most pressing challenges. FNZ has also created strategic partnerships to help drive change, including Benchmark for Nature, a partnership with Oxford University to enable investors to understand the impact of their investments on nature, and Big Issue Invest, a partnership with The Big Issue to power a new investment platform that brings environmental funds direct to the retail consumer.

Task Force

Integration into our overall risk management

The investment philosophy and process we have described is the primary way that we mitigate climate-related risks across the firm. The firm is built on the premise that climate change will be a significant driver of economics and a source of both risk and opportunity. In this way, it is built into the fabric of the firm and not a separate agenda topic or applied to a separate proportion of our assets.

However, we also embed climate risks into the firm's overall risk management framework, for which our Senior Partner and Management Committee have ultimate responsibility. The operation of the infrastructure group, as well as certain regulated activities, is overseen by the Risk Oversight Group (ROG), which is chaired by a Non-Executive Officer. The ROG reports to the Management Committee. Generation's risk management framework and governance structure are intended to provide comprehensive controls and ongoing identification and management of its major risks. The ROG meets regularly to review internal controls, risk management processes, regulatory compliance and relevant reports received from Generation's advisors and auditors. While climate change risk is not considered a major internal risk, the ROG’s annual deliverables include reviewing and monitoring the firm’s carbon-neutral status while on the journey to net zero emissions and ongoing compliance with all relevant regulations. This includes reviewing updates on potential climate-related risks to operations.

Metrics and targets

Generation has sought to report on a wide range of environmental metrics for years, in an effort to understand both the climate-related risks our portfolios are exposed to as well as the positive opportunitie we might pursue. The TCFD recommendations on metrics formed the basis for important dialogue across our firm on how to provide robust, best-in-class disclosure to our investors. At the same time, we are conscious that the methods and data required to evaluate climate exposure are still evolving, and as such we are always looking to use the most robust and forwardlooking approaches.

Metrics and sustainability measurement

Since 2018, we have undertaken regular comparative analysis of our listed equity strategies against their benchmarks on a range of ESG metrics, as a check on the outcomes of our investment and stewardship process. We also provide select climate-related metrics alongside other ESG and financial metrics for the Global Equity portfolio as of 15 March 2021 below. The Benchmark represents the MSCI World Index.

Furthermore, we also analyse the Scope 3 emissions associated with our Global Equity portfolio. Beginning in 2019, we began performing deep dives into Scope 3 emissions of our Focus List companies, over half of which report Scope 3 data to the Carbon Disclosure Project. However, the quality of Scope 3 reporting is highly inconsistent, and we therefore need to use modelled estimates which have well-known limitations. It is, however, clear that Scope 3 emissions are much larger than Scope 1 and 2 in most cases – as a general guide, for over 90% of our Focus List, Scope 3 accounts for more than 80% of total emissions. We have identified over 30 companies in the Focus List that we prioritise for engagement on climate change, selected for their failure to disclose emissions, the scale of their Scope 1 and 2, or Scope 3 emissions, or their potential to make early progress and/or have a positive system impact.

Engaging on Scope 3 emissions is potentially complex. The good news is that data availability is improving and there is a growing body of best practice. Frameworks for target setting are also more established today than they were just a few years ago. Over 30% of companies in our Focus List have joined the Science-Based Targets initiative, which requires them to set targets to reduce material Scope 3 emissions alongside Scopes 1 and 2.

Asia Equity

As we do for Global Equity, we provide select climate-related metrics alongside ESG and financial metrics for the Asia Equity portfolio as of 15 March 2021 below. The Benchmark represents the MSCI All Country Ex-Japan.

Growth Equity

For our Growth Equity strategy, we are in the midst of publishing our third Sustainability Report for Sustainable Solutions Fund III, with a more detailed report to be made available to clients. Sustainable Solutions Fund III, with ~USD 1 billion of committed capital, is our largest Growth Equity fund to date. This year’s report covers a full year of outcomes from the eight companies we held in the portfolio as of 31 December 2020.

In our reporting, we focus on measuring outcomes (i.e. the effects of outputs on an issue we aim to address) as opposed to outputs themselves (i.e. what a company’s activity produces). We measure these outcomes across the three thematic areas of focus for the fund: Planetary health, people health and financial inclusion. While our companies are still young and at different stages of their ability to prove their impact, we aim to present aggregate portfolio data across these three outcome dimensions.

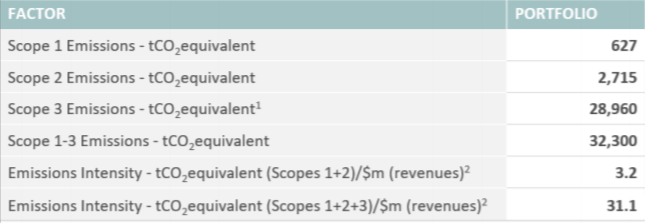

In addition to our Sustainability Report, we provide select metrics on the absolute emissions and emissions intensity of our portfolio. Please see below the results for Sustainable Solutions Fund III’s eight companies that were in the portfolio as of 31 December 2020:

Metrics and targets

Finally, we have chosen to provide standardised reporting aligned with the Sustainability Accounting Standards Board (SASB) standards, a framework designed to assist companies in disclosing financially material, decision-oriented sustainability information to investors. We believe this level of disclosure is best practice for our private companies as they mature. We also provide analysis to support our clients’ interest in mapping outcomes to the Sustainable Development Goals (SDGs) as well as the five dimensions of the Impact Management Project (IMP). Lastly, we look to provide colour with real case studies, in some instances powered by customer surveys to benchmark how each company is improving quality of life for its stakeholders.

Our target: Net zero by 2040

Our target is to achieve net zero emissions across all the investment strategies we manage by 2040 or sooner, and is therefore an absolute emissions reduction target. The baseline for our commitment is 2019. In line with our commitment to the Net Zero Asset Managers initiative, we will set interim targets for 2030 consistent with a fair share of the 50% global reduction in CO2 identified as a requirement in the IPCC special report on global warming of 1.5 degrees Celsius. We expect to continue to use implied temperature rise analysis, an intensity-based metric, as our primary metric to assess progress against our targets, while also continuing to track the reduction of portfolio emissions intensity over time.

We are committed to achieving net zero emissions in our business operations on the same timescale as outlined above. We are working with external consultants on understanding more deeply all material aspects of our operational emissions and the levers we have, establishing interim targets, and determining how to track progress

Long-term Equity

As mentioned above, our Long-term Equity strategy holds one portfolio company, FNZ. Please see the 2020 carbon absolute emissions and emissions intensity results for FNZ below. Further detail on FNZ’s climate impact will be made available on their website this year, as part of their sustainability report.

The path ahead

We recognise there is much more work we need to do to see our vision for sustainable investing and sustainable capitalism realised. In parallel, we recognise there is much required to strengthen and enhance climate-related risk and opportunity assessment, which is an essential building block of a sustainable transition.

In our own practice, we aim to expand our measurement and monitoring of key metrics across all strategies, and to explore systematic, portfolio-level analysis of our exposure to physical climate and transition risks under different scenarios. We will also continue to support the development of best-in-class tools and expanded emissions disclosure and data availability, such as through our ongoing involvement in the Portfolio Alignment Team, a cross-firm coalition dedicated to identifying best practice in measuring portfolio alignment, and through our Senior Partner’s continued support of the TCFD.

We will continue to advance how we manage climate risk and accelerate investments towards the climate transition. For example, we will continue to leverage our engagement and proxy voting capabilities to elevate the ambition and action of our portfolio companies, and we will continue to support a focused range of impact and advocacy initiatives in an effort to galvanise transformation across our industry. Furthermore, as we already do, we will not only monitor and mitigate climate-related risks, but also continue to invest in companies that we believe can accelerate solutions to climate change and mitigate climate risk exposure for all.