Felix Preston

Felix Preston

Felix Preston

Felix Preston joined Generation Investment Management in 2019 and is Director of Sustainability Impact and Research. Previously, Felix worked as a deputy research director and senior research fellow at Chatham House (The Royal Institute of International Affairs), where he led the energy, environment and resources department’s work on innovation and disruptive change. Felix also worked at AEA Technology, the Environment Agency and Safe Neighbourhoods Unit.

Felix received a BSc in Environmental Science and Geography from the University of Sussex and an MSc in Environmental Technology – Energy Policy from Imperial College London.

Ida Hempel

Ida Hempel

Ida Hempel

Ida Hempel joined Generation Investment Management in 2019 and works in investments and as part of the founding team of Just Climate. Prior to Generation, Ida worked in investments at the Emerson Collective and in consulting at Boston Consulting Group.

Ida received an MBA and MS in Environment and Resources from Stanford University and a BA from Harvard University.

In brief

- Many climate discussions focus on the finance gap, but there is no shortage of capital available for the net zero transition. We need more attention on closing the ‘Impact Gap’, so capital can be deployed at the right time, in the right places and in sufficient volumes.

- The Impact Gap poses a major risk to the world and to sustainable investment. The solutions for 50% of global emissions receive around 10% of the capital flowing into climate finance.

- Key drivers of the Impact Gap include concerns over the quality of climate-related investment and the challenges of transitioning systems to net zero.

- In this Insights piece, we identify the critical innovations urgently needed to close this Impact Gap and add new momentum to climate action on the road ahead from COP26.

Introduction

Limiting the global temperature rise to 1.5 degrees will require an investment of $3 trillion per year to 2050, according to the IPCC.1 Other estimates are even higher, especially when protecting biodiversity and ensuring a just transition are included.

This investment is essential, will bring many co-benefits, and is dwarfed by the cost of inaction. Nevertheless, it is a daunting task. Climate solutions will need to be deployed at unprecedented rates over the next decade. Today, investment in clean energy is running at around $0.5 trillion per year.2

For all the talk of a climate finance gap, there is no shortage of capital ready to be deployed behind net zero. In recent months, the total value of assets held by managers with net zero commitments has risen to $57 trillion, more than half of all capital under management. Firms representing $130 trillion of assets now belong to the Glasgow Financial Alliance for Net Zero.3 In crude terms, this is more than enough to invest $3 trillion per year to 2050, even before value addition is considered.

Instead, we should be more worried about the looming Impact Gap. This is the risk that capital is not deployed at the right time, in the right places, in sufficient volumes, while addressing equity concerns. If this gap is not closed, we will miss the 1.5 degree goal despite having sufficient funds in play – a failure that future generations are unlikely to forgive.

To close the Impact Gap, there must be more focus on the quality of climate action, alongside the well-known challenges of scaling up. How can it be, for instance, that the ESG sector is managing trillions of dollars, yet global emissions continue to rise? Why are emissions not reducing in step with the proliferation of net zero commitments? In this Insights piece, we highlight several quality issues and systemic challenges that must be tackled.

The Impact Gap threatens to derail climate action in the coming months and years, but it can and must be addressed. Doing so will ensure not only that climate solutions reach sufficient scale, but also that they are applied everywhere they are needed in time to avoid catastrophic climate change. In the concluding section of this piece, we set out four critical innovations that can close the Impact Gap.

Understanding the Impact Gap

The scale of the challenge

Reaching net zero by mid-century, which is required for a 1.5 degree pathway, means ramping up myriad solutions across every sector and geography. Much of the focus will fall on energy, which today drives around 40% of global emissions, but similar transformations are needed in industry (~20%), mobility (~25%), buildings and in activities related to land use.4

Certain solutions, such as renewables and clean hydrogen, can enable the transition across all sectors, as processes and end-use applications are electrified or shift to clean fuels. At the same time, almost a quarter of emissions reductions will come from decarbonising the hardest-to-abate areas such as cement, steel, plastics, heavy road transportation, shipping and aviation, which require a wide range of supply- and demand-side changes and substitutions.5 Nothing short of a transformation of our built environment and energy system will suffice.

Today, we fall short on many fronts – sometimes by an order of magnitude. The IEA estimates that by 2050, over 80% of electricity will be from renewable sources.6 To achieve this, the pace that we add new capacity in wind and solar each year must increase by three and five times respectively, as you can see in the charts below. Similarly, despite positive momentum around electric vehicles, their share of global car stock must increase by a factor of 20 in the next decade – and over 80 times by 2050. A similar story is unfolding around other key solutions that are in earlier stages, including the deployment of zero carbon ready buildings, CO2 capture and removal, sustainable natural solutions and clean hydrogen production.

Figure 1: The rate of deployment must hugely increase for a 1.5 degree pathway

Source: IEA7

Investing in the right solutions, at the right time

Let’s consider what closing the impact gap means for investment in climate solutions.

While the exact path to achieving net zero is uncertain, various sources indicate that investment in relevant areas will rise to the tens of trillions over the next three decades. The IPCC suggests that supply-side investments must reach $1.6 to $3.8 trillion per year, on average, to 2050.8 The Energy Transitions Commission estimates $1.5 to $1.8 trillion of investment will be needed each year up to 2030 across power, hydrogen, industry and transport.9

These estimates don’t include the substantial investments required for other demand-side transformations, land use and agriculture, carbon capture and adapting to climate change, among many other things. McKinsey, for example, estimates it will take annual capital flows of $100 billion into nature-based solutions to realise these solutions’ full potential.10 The true total will therefore be far greater.

Figure 2: Key investment needs for net zero

| 2050 vision | Key investment needs | Total investment 2020-2050, US$bn | Total annualised investment, US$bn | ||

| Power |

Total power generation:

|

Renewable capacity | 9 TW extra onshore wind 3 TW extra offshore wind 18 TW extra solar |

~32,000 | ~1,000 |

| Transmission and distribution | 3-33% of generation capacity investment | ~1,000-10,000 | ~30-350 | ||

| Battery storage | 14 TWh per day (5% of daily generation) | ~1,500 | ~50 | ||

| Seasonal storage: H2 storage and/or CCS on thermal plants | 4 TW thermal capacity equipped with CCS (8% of generation) | ~3,800 | ~130 | ||

| 1.5 TW electrolysis (2% power shifted) | ~430 | ~15 | |||

| Hydrogen in final use | 800 Mt/year for final sectoral energy use | Production | 5.8 TW electrolysis 2 TW blue hydrogen capacity |

~2,600 | ~90 |

| Transport and storage | Salt caverns and other storage Gas pipeline retrofit |

~1,100 | ~40 | ||

| Industry | Steel, cement and petrochemicals industries achieve zero-carbon | CCS application to cement Hydrogen DRI or CCS for steel Multiple forms of changed chemical production process |

~1,600 | ~50 | |

| Transport: charging infrastructure | Total decarbonisation of road transport with ~2bn electric trucks and buses | ~1000bn slow residential, 200m moderate speed public and 10million superfast chargers, + truck and bus chargers | ~2,000 | ~70 | |

| Total | ~46,000-55,000 | ~1,475-1,800 | |||

| CCS across all sectors (included in figures above) | 6-9.5 Gt/year of gross emissions from power, hydrogen production and industrial sectors (excluding feedstock) offset by CCS/U | Capture equipment, transport pipelines and storage facilities | ~4,800-5,600 | ~160-190 | |

Source: Energy Transitions Commission (2020)11

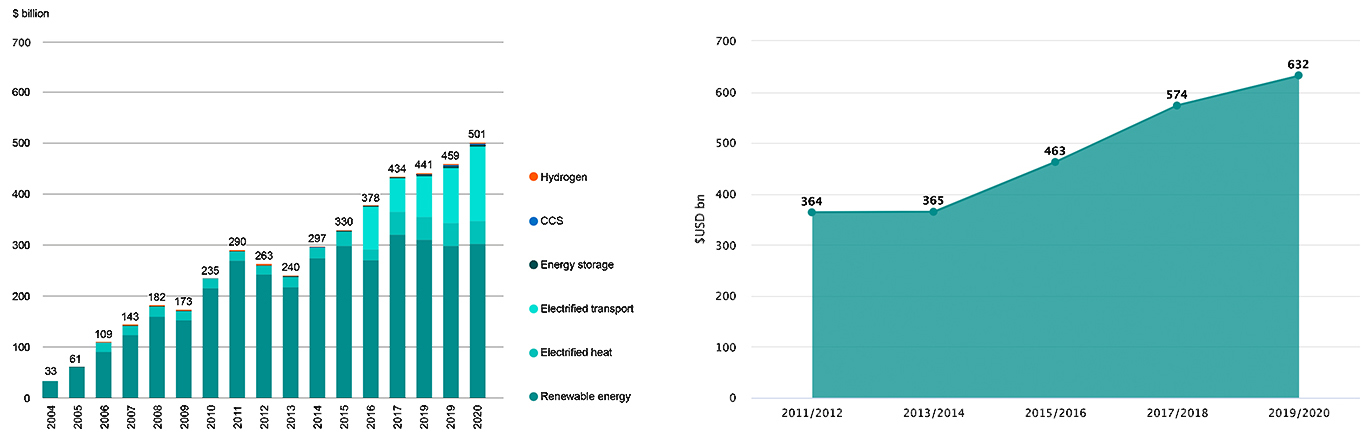

Today, the volumes of capital flowing into net zero-aligned solutions fall well short of these levels. The Climate Policy Initiative estimates that investment into aligned solutions reached $632bn across public and private sources in 2019/2020.12 BloombergNEF estimates that global investment in the energy sector (inclusive of carbon capture, hydrogen and electrified transport) reached around $500bn in 2020.13 Inflows into climate solutions must grow by three to eight times in order to meet global climate goals.14

Figure 3: Energy transition investment (left) and climate finance (right)

As we noted above, investors are not allocating capital according to the greatest potential for impact. Climate finance is currently focused in a few crucial areas, such as renewables, electric vehicles and LED lighting. These are crucially important, but we cannot get to a 1.5C pathway without a full-spectrum approach that spans hard-to-abate solution areas and geographies. Investment flows into climate solutions must go both deeper and broader.

We estimate that solutions with the potential to address 50% of global emissions receive around 10% of the capital flowing towards climate finance17 – a ballpark figure based on research for our investment roadmaps. Scaling up solutions in cement and steel (~7-8% of global emissions each), aviation and shipping (~4% of global emissions combined), and complementary nature-based solutions such as sustainable forestry and regenerative agriculture (with the potential to abate 20%+ of global emissions18) could, in aggregate, reduce approximately half of global emissions today. And yet, we estimate that these same hard-to-scale and hard-to-abate areas receive around $55bn annually – roughly 10% of the $632bn the Climate Policy Initiative estimates is flowing to climate solutions across asset classes and sectors. These are some of the areas with the highest potential climate impact –yet they attract the least capital.

Just as concerning is the distribution across geographies. Most solutions, from electric vehicles to clean hydrogen production, are being deployed in the developed world and in China. The OECD estimates that climate finance for developing countries was around $80bn in 2019.19 Some of the widest gaps persist in areas with the greatest and timeliest impact potential, such as parts of Africa, South and Southeast Asia and Eastern Europe, which continue to rely heavily on coal-powered generation, with its associated health impacts.

Of course, we also need to deliver clean technologies at the right time. Our Time Value of Carbon insights piece explains why cuts in greenhouse gas emissions today are worth more than cuts promised in the future, due to the escalating risks associated with the pace and extent of climate action.20 In its latest Emissions Gap Report, the UN Environment Programme highlights the risk of waiting until 2030 before steep cuts begin.21

Key drivers of the Impact Gap

Valid questions are being raised about the impact claims of ESG and thematic climate investment strategies, some of which appear to deliver only marginal benefits at best. Since 2015, we have observed an almost twentyfold increase in ESG-aligned AUM, while annual flows into ESG funds have increased by about ten times.22

Clearly, we have not observed a similarly rapid scale-up in the allocation of capital to climate solutions. Investment in the energy transition has grown 1.7x in that same period, and we have observed only a 2x increase in PE/VC deal flow in the sustainability space.23 While not all ESG assets will necessarily have an explicit climate focus, this wide disparity suggests the impact of much of today’s environmentally oriented ESG assets is limited.

Figure 4: Flows into ESG funds and historical AUM

Source: Bloomberg Intelligence24

We believe that the Impact Gap is caused by two sets of factors in particular. First, the understandable focus on the quantity of climate solutions has led us to downplay the importance of quality and integrity. Second, the systemic nature of the problem poses particular challenges that we are only now beginning to tackle.

Quality and integrity

Three interlinked quality issues are contributing to the Impact Gap. Together, these lessen the positive impact of the solutions being deployed, while simultaneously acting as barriers to any further scale-up.

First, as we noted above, the soaring interest in ESG funds and indexes is not yet driving a commensurate real-world impact on decarbonisation. This suggests that fundamental quality issues remain around capital allocation, despite the mainstreaming of sustainable finance in recent years. It’s as if the cogs are turning but the machine is not in gear. Capital flows are concentrated in a few technologies and geographies while other areas are starved of investment – something is clearly wrong in the capital allocation process.

Second, most claims about climate impact involve a forward-looking dimension. This includes setting targets for net zero and allocating capital to low-carbon goods, services and infrastructure which promise to deliver future carbon reductions. Investors must therefore consider not only a company’s long-term goal, but the credibility of its plan to meet it.

Focusing more on the future is a welcome development, but it brings new challenges. For instance, the issues around setting net zero targets are discussed in our Insights paper on the topic.25 It is critical that consistent, high-quality approaches to setting and disclosing net zero goals for both corporates and investors are agreed. In particular, we must be able to evaluate whether near-term action is setting organisations on a credible path to net zero.26

The third ‘quality’ issue is the credibility of claims made about carbon sources and sinks. These have both temporal and spatial dimensions. For nature-based solutions, for instance, it takes time for carbon dioxide to be absorbed into trees and other vegetation. A landscape being reforested might sequester carbon at a rate of around 10 to 20tCO2 per hectare per year over the first 20 years.27 Problems arise when claims are made about carbon removals from nature that will take years to achieve and then used to offset current activity. Put simply, planting a tree today that will absorb carbon over decades is not a fair ‘offset’ for your company’s flights last year.

An even harder question is whether that carbon removal would have happened in the absence of the investment. Challenges in assessing ‘additionality’ have been well-documented, while the permanence of carbon storage in vegetation and soils is also hard to assess. Equally, the impact of nature-based solutions on biodiversity, water and human livelihoods must be considered alongside carbon considerations. The assumptions used to evaluate the impact of climate solutions in these areas are important and contentious, especially when organisations plan to claim them as ‘removals’ in their net zero plans.

Carbon sinks and sources do not only arise in the context of nature-based solutions. The new 2050 net zero plan for the cement and concrete sector, for instance, includes a chunk of carbon removal, because concrete slowly absorbs some carbon from the atmosphere.28 The use of geological carbon storage also raises questions about permanence and governance.

Systemic factors

Several systemic and structural factors contribute to the Impact Gap, many of which are mutually reinforcing.

First, there is an information barrier: many investors and emitters have limited knowledge of how to achieve net zero in their companies or portfolios. Transition plans require technical or regulatory expertise that institutions often do not have in-house. Indeed, plans for certain areas simply may not yet exist – the playbook for hard-to-abate areas such as cement, steel and some other industries is still to be defined. This information barrier drives both the quantity and quality aspects of the Impact Gap. Even capital allocators that seek to get involved struggle to do so, due to insufficient data or a lack of experience in delivering the highest-quality investments in these spaces.

Furthermore, achieving net zero in many sectors is a systems challenge, requiring progress to be made at multiple levels for net zero-aligned business models to make sense. There are many interdependencies between solutions, such as where several technologies need to come down the cost curve in parallel, or the co-evolution of applications and use cases is beyond a single company’s control. Scaling green hydrogen is a case in point: the supply-side economics will depend on continuing cost declines in renewables and electrolysers over the next decade, which need to continue to scale at a double-digit rate. On the demand-side, while hydrogen has many potential applications across industry, mobility and power, many use cases have yet to mature, and sources of long-term offtake for hydrogen projects remain challenging to secure. All of these factors create further friction in decarbonising hydrogen production in general, and demand even greater commitment and creative persistence on the part of participants.

There is also a systematic mismatch between the capabilities of today’s capital markets and what is required for a 1.5 degree pathway. We need to expand what capital markets value by incorporating impact within a traditional risk and return framework. Investors will otherwise remain hesitant to invest due to the complexity of decarbonisation solutions and the unknown regulatory outlook. Investing in net zero-aligned solutions requires an assessment of climate impact as a value driver.

Impactful climate opportunities often have high-risk elements, resulting from commercialisation uncertainty, market dynamics, regulatory uncertainty or exposure to carbon markets – all of which may cause these companies and projects to fall outside of investors’ existing mandates.

As a result of all these factors, there are few funds with meaningful track records in the areas that most require further investment, and there remains a collective lack of expertise in how to take these unconventional risks.

Innovations to overcome the Impact Gap

Bridging the Impact Gap is possible, but we believe innovations are required in four areas: data and measurement; investment mandates and capital allocation strategies; increased allocation of capital towards climate transition, including new sources of capital; and policy frameworks and accountability for net zero. We outline these areas below:

- Aligning portfolios with net zero. Asset managers need new processes to interpret the best available climate science and identify the opportunities required for deep decarbonisation. It will be important to overlay investment processes with an authentic understanding of the viable pathways to net zero, how different solutions interact and potential systems effects. Asset managers will also need to revisit the metrics on which they are tracked and incentivised. This presents an opportunity for asset owners to differentiate between greenwashing, ’light green‘ and ’deep green‘ strategies.

- Innovation in investment mandates and strategies. We need to unlock the flow of capital into the full spectrum of deep decarbonisation opportunities. This is likely to require new types of investment mandates and impact-focused strategies. To tackle complex risks in under-invested areas, we will need scalable models for blended finance.28 These enhanced impact strategies can be coupled with the advanced analytics envisaged in ‘aligning portfolios with net zero’ to ensure the Impact Gap is closed.

- New sources of capital. Recent months have seen companies step forward with multi-billion dollar plans to invest in nature and deep decarbonisation. There has also been an explosion in green bonds, which are becoming ever more credible as verification processes improve. We see a growing role for retail investors, for communities that join together to invest in sustainable energy, and for communities that live and work in regions offering nature-based solutions. This flow of impact-focused capital will be a crucial source of impetus for the new kinds of investment mandates we highlight above.

- Innovation in policy frameworks. Governments have a key role to play in setting incentives, whether through carbon prices and technology standards or due diligence in supply chains. State-owned and multilateral investment banks will also play an important role in de-risking complex projects. Finally, investors and companies alike need to be held to account for their net zero claims – the institutions that conduct this work will need further strengthening, based on the most rigorous, science-based approaches

Conclusion

Closing the Impact Gap is a critical priority for investors, governments and other stakeholders. We need to scale up the volume of climate solutions in all geographies. At the same time, we need to enhance the quality of climate impact.

This is an enormous challenge. In this Insights piece, we set out four innovations required to address the impact gap. The good news is that progress is beginning to emerge in each of these areas.

As discussions at COP26 underscored, immediate action is required to cut CO2 emissions in half by 2030 and keep a 1.5 degree pathway within reach. Closing the impact gap is now our collective task. There is much work to do.

- IPCC (2019). ‘Special Report: Global Warming of 1.5C’. See page 321.

- BloombergNEF (2021). ‘Energy Transition Investment Hit $500 Billion in 2020 – For First Time’. See article.

- See GFANZ announcement at COP26

- IEA (2019). Global CO2 emissions by sector, 2019. See data

- SYSTEMIQ Analysis for the Energy Transitions Commission (2018). ‘Mission Possible’. See report.

- IEA (2021), ‘Net Zero by 2050: A Roadmap for the Global Energy Sector’. See report.

- IEA (2021), ‘Net Zero by 2050: A Roadmap for the Global Energy Sector’. See report

- McCollum et al. (2018), ‘Energy investment needs for fulfilling the Paris Agreement and achieving the Sustainable Development Goals’. See paper

- SYSTEMIQ Analysis for the Energy Transitions Commission. Making Mission Possible – Delivering a Net-Zero Economy (2020). See page 54 of the report

- Assuming an illustrative $20/t carbon price. McKinsey (2021). Why Investing in Nature is Key to Climate Mitigation. See report.

- SYSTEMIQ Analysis for the Energy Transitions Commission. Making Mission Possible – Delivering a Net-Zero Economy (2020). See page 54 of the report

- Climate Policy Initiative (2021). ‘Global Landscape of Climate Finance’. See report

- BloombergNEF (2021). ‘Energy Transition Investment Hit $500 Billion in 2020 – For First Time’. See article.

- Generation analysis.

- BloombergNEF (2021). ‘Energy Transition Investment Hit $500 Billion in 2020 – For First Time’. See article

- Climate Policy Initiative (2021). ‘Global Landscape of Climate Finance’. See report

- This indicative statistic is based on the following calculation: a) Estimates of financial flows into harder to abate sectors are aggregated from multiple sources, including Energy Transitions Commission, IEA, CB Insights and the Climate Policy Initiative. Generation has analysed each of these sectors in recent internal investment roadmaps. In most categories we believe current annual investments are less than $1bn per sector, with the exception of buildings and infrastructure and certain areas of land use and agriculture, where we use Climate Policy Initiative estimates. We divide this by total climate finance of around $632 billion, the estimate from Climate Policy Initiative, to arrive at around 10% of total climate finance flows. b) Emissions data for hard to abate sectors is based on Energy Transition Commission (~10 GtCO2e). We combine this with the IEA’s estimates of total emissions from the buildings sector (~7 GtCO2e) and the Griscom et al. (2017) estimate of cost effective abatement potential from nature based solutions (~11 GtCO2e), although strictly this is an estimate for annual potential in 2030. In total this comes to around 50% of global emissions today, using 57.4 GtCO2e as the denominator (PBL Netherlands Environmental Assessment Agency).

- Griscom (2017). ‘Natural climate solutions’. PNAS October 31, 2017 114 (44) 11645-11650. See article

- OECD (2021). See statement

- See Generation Insights piece on the Time Value of Carbon

- UNEP Emissions Gap Report (2021). See report

- See Figure 1 in Generation (2021), ‘Sustainability Trends Report 2021’. Data underlying analysis from CB Insights, Bloomberg, BNEF, Reuters and FTSE Russell.

- See Figure 1 in Generation (2021), ‘Sustainability Trends Report 2021’.

- Bloomberg (2021). ‘ESG assets may hit $53 trillion by 2025, a third of global AUM’. See article

- Race to Zero – Generation IM Insights piece.

- TCFD (2021), ‘Task Force on Climate-related Financial Disclosures Guidance on Metrics, Targets, and Transition Plans’. See report. See also SBTi’s ‘Net Zero Standard’, available here.

- Bernal, B., Murray, L.T. & Pearson, T.R.H. Global carbon dioxide removal rates from forest landscape restoration activities. Carbon Balance and Management 13, 22 (2018). See website.

- See the Global Cement and Concrete Association roadmap

- See this call for blended finance from the Net Zero Asset Owners Alliance

Important Information

The ‘Insights 07: The Impact Gap' is a report prepared by Generation Investment Management LLP (“Generation”) for discussion purposes only. It reflects the views of Generation as at November 2021. It is not to be reproduced or copied or made available to others without the consent of Generation. The information presented herein is intended to reflect Generation’s present thoughts on sustainable investment and related topics and should not be construed as investment research, advice or the making of any recommendation in respect of any particular company. It is not marketing material or a financial promotion. Certain companies may be referenced as illustrative of a particular field of economic endeavour and will not have been subject to Generation’s investment process. References to any companies must not be construed as a recommendation to buy or sell securities of such companies. To the extent such companies are investments undertaken by Generation, they will form part of a broader portfolio of companies and are discussed solely to be illustrative of Generation’s broader investment thesis. There is no warranty investment in these companies have been profitable or will be profitable. While the data is from sources Generation believes to be reliable, Generation makes no representation as to the completeness or accuracy of the data. We shall not be responsible for amending, correcting, or updating any information or opinions contained herein, and we accept no liability for loss arising from the use of the material.